Press Story

Big Tech must open up data and help fund digital inclusion as UK economy moves away from cash in 2020s, says IPPR

- New competition powers should compel big digital firms to share their data if they enter personal finance market - to prevent market domination and promote innovation

- As UK heads to a ‘less cash, but not cashless’ digital economy, UK must step up investment in digital skills and connectivity to meet new inclusion targets

In a comprehensive review of the future of UK payments, the think tank IPPR has set out how the transition to a ‘less cash’, but not cashless, digital economy can be managed to protect the vulnerable and spread digital opportunities widely and fairly.

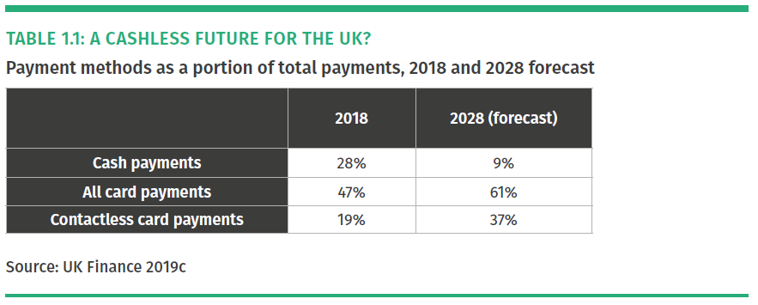

The digital transition is already happening fast. While in 2008 60 per cent of UK consumer payments were made in cash, this had fallen to just 28 per cent in 2018. The IPPR report cites forecasts that by 2028 fewer than one in 10 payments will be made in cash.

The digital revolution in finance means a shift to a considerably less cash-based digital economy, but the prospect of a fully cashless UK is not on the horizon, argues IPPR. This shift is expected to boost UK productivity and create opportunities for business and consumers, but there is a significant risk that people and areas reliant on cash may be excluded.

Giant tech firms such as Facebook and Amazon are already starting to offer more personal financial services, alongside traditional banks, but the control they could have over huge amounts of people’s data poses significant risks.

The IPPR report argues that as cash use continues to fall and digital payments break new ground, it is critical that policymakers take action to shape the future of UK payments. To deliver a future that is both more digital and more just, IPPR recommends:

- Major platforms such as Facebook and Amazon should be required to open up their data upon entry into the personal finance market. New powers should enable the Competition and Markets Authority (CMA) to impose conditions on market entry for major platforms, including requirement to comply with Open Banking principles and open-source technology. These should include an option to block market entry, including for major technology platforms, where it could lead to consumer detriment, slowing in innovation rates, or excessive market power.

- Democratising data - Anonymised personal banking and financial service data should be held in a new public data trust, ‘Digital Britain’. This will strengthen competition, promote innovation and prevent monopolistic tech giants dominating the market.

- Digital Transition Levyworth billions of pounds a year – Reforming the Banking Levy on banks and financial service providers to fund the delivery of digital inclusion schemes against new digital inclusion targets – boosting internet connectivity, strengthening digital skills and fostering innovation that will help people overcome the barriers to the digital economy. The new levy combined with new targets would mean that those who stand to gain most from the digital transition will have some of their gains reinvested in communities that risk being left behind.

- Bridging the digital divide - More than 8 million UK adults still rely on cash and one in five people do not yet have the digital skills they need to access the digital economy. New targets and investment should be put in place to protect cash access for those who rely on it and to narrow the digital divide across the UK.

- Protecting long-term access to cash – Between 2017 and 2018 6,243 cash machines have been closed – a 9 per cent drop in a single year. While there are still more UK ATMs in operation than at any point before 2006, this recent rate of decline is a cause for concern. To stem the decline of free-to-use ATMs, business rate rebates should be offered to operators who provide them, and retailers should be incentivised to roll out free cashback services.

- Creating a new Post Bank – Between January 2015 and August 2019, 3,312 bank and building society branches closed in the UK, equivalent to 55 closures a month. The UK Treasury should oversee the creation of a publicly owned Post Bank with a public service mandate to provide basic banking services to all citizens. It would operate via the existing Post Office network and help ensure the future viability of the Post Office.

- Championing digital self-employment – The government should develop a digital platform for self-employed workers, so they can better manage payments, streamline tax accounting and apply social security provision. This will not only save them time and boost tax revenues, but also help tackle fraud and financial crime by bringing the informal economy into the system.

IPPR argues that these proposals, amongst others in the report, will deliver a path to a digital economy that delivers not just greater prosperity, but greater economic justice: where more people can access better payments and banking services, data is harnessed for the public good and the most vulnerable people are protected.

The report notes that an increasingly digital economy brings faster payments, more personalised services and greater convenience for digital users. However, if these benefits are only available to digitally savvy people – typically younger people and those with higher incomes - inequality could be embedded into the future of finance, it warns.

IPPR urges the government to seize this moment to prevent all the gains from digitisation flowing to big tech firms and big finance and instead deliver excellent financial services for all, a competitive innovative personal finance market and democratic control of data.

Rachel Statham, IPPR Economic Analyst and lead report author, said:

“The future will have less cash. But urgent action is needed to set the UK on course towards an economy that is both more digital and more just. By getting ahead now, we can invest the billions needed to get every part of the country ready for a more digital future and protect access to cash where people rely on it. This could see the potential benefits brought by a move away from cash invested to narrow rather than widen inequalities, handing control over from Big Tech and banks to people and communities.

“The move away from cash should only happen as fast as people are ready for, and the benefits of doing so should be shared. By setting new digital inclusion targets at the national, regional and local level, and investing to meet these targets, we can make sure bridge the digital divide and protect cash for those rely on it.”

Carys Roberts, head of the Centre for Economic Justice and IPPR Chief Economist, said:

“There are opportunities within reach as the UK economy shifts away from cash and towards digital payments – from productivity increases to preventing fraud and financial crime. But there’s also a danger that the shift to digital, if not proactively shaped, will work for some and leave many behind. The government should enable everyone to take part in the digital economy and ensure powerful companies like Apple and Google play their full part in shaping a fairer move away from cash in the UK.”

ENDS

NOTES TO EDITORS

- The IPPR paper, Not Cashless, But Less Cash: Economic Justice and the Future of UK Payments by Rachel Statham, Lesley Rankin and Douglas Sloan, will be published at 0001 on Friday 24th January 2020. It will be available for download at: http://www.ippr.org/research/publications/not-cashless-but-less-cash

- Advance copies of the report are available under embargo on request.

- UK Finance projections estimate that by 2028 just 9 per cent of UK payments will be made in cash. For more detail see UK Finance UK Consumer Payments 2019.

- IPPR’s research drew on focus groups conducted with consumers in Tongwynlais in the South Wales valleys, Peterborough in South East England, and Inverness in the Scottish Highlands.

- Fig 1.1: The pace of transition to digital payments has not been uniform across the UK

- Table 1.1: UK Finance forecasts for future of payment methods (2019)

- IPPR is the UK’s pre-eminent progressive think tank. With more than 40 staff and offices in London, Manchester, Newcastle and Edinburgh, IPPR is Britain’s only national think tank with a truly national presence. www.ippr.org